CTFS Announces FY2026 Interim Results

- Progressive Growth with a Solid Financial Foundation -

26.02.2026

(26 February 2026, Hong Kong) CTF Services Limited (the “Company” and its subsidiaries, collectively, “CTFS” or the “Group”; Hong Kong stock code: 659) today announced its interim results for the six months ended 31 December 2025 (the “Current Period” or “1HFY2026”).

HIGHLIGHTS

Mr Brian Cheng, Executive Director and Group Co-Chief Executive Officer of CTFS, said, “CTFS has delivered resilient performance with solid growth, underscoring the strength of our diversified business portfolio. We are advancing in our Financial Services and Logistics segments, with recent acquisitions driving strategic expansion and strengthening our market position, marking key milestones in our roadmap. We remain focused on strengthening portfolio resilience and maximizing synergies with the Chow Tai Fook Group, while seizing quality growth opportunities at the right time to drive sustainable, long‑term value creation.”

Mr Gilbert Ho, Executive Director and Group Co-Chief Executive Officer of CTFS, added, “CTFS will continue to pursue disciplined growth, anchored by prudent approach to capital and risk management. Backed by a strong balance sheet and commitment to operational excellence, we are well‑positioned to navigate evolving market conditions. By optimizing our portfolio and enhancing efficiency, we reinforce cash flow resilience and deliver stable performance, enabling us to uphold a sustainable and progressive dividend policy across market cycles.”

Disciplined Capital Allocation

Strategic Divestment and Acquisitions

The Group applied a disciplined approach to capital allocation, balancing strategic divestments of stagnant assets and targeted investments in areas of clear strategic importance. In October 2025, the Group monetized its investment in Shoucheng Holdings Limited under the Strategic Investment segment through the issuance of HK$2,218 million 0.75% exchangeable bonds due 2028 (the “0.75% Exchangeable Bonds”). This transaction enables the Group to diversify its funding source and strengthen its financial flexibility to support future growth initiatives while potentially divest the investment with an attractive return.

The Group also advanced selective acquisitions to reinforce its core business segments, including the following:

Financial Services:

Logistics:

Proactive Financial Management Strengthens Liquidity

Strengthening Liquidity and Reducing Leverage Level

The Group maintains a solid financial position. As at 31 December 2025, total available liquidity amounted to approximately HK$31.0 billion, comprising cash and bank balances of approximately HK$20.9 billion and unutilized committed banking facilities of approximately HK$10.1 billion, comfortably exceeding near-term maturities. As at 31 December 2025, net debt declined to approximately HK$13.8 billion (30 June 2025: approximately HK$14.7 billion), with the net gearing ratio, calculated as net debt over total equity, further edged down to 34%1 (30 June 2025: 37%). The Group reduced its average borrowing costs to approximately 4.0% per annum (for the six months ended 31 December 2024 (the “Last Period”): 4.2% per annum).

During the Current Period, the Company successfully increased its public float to meet the regulatory requirement. In July 2025, the Company issued HK$850 million of 2.80% convertible bonds due 2027. Subsequent conversions lifted public float to approximately 25.08% as at 21 November 2025, complying with the minimum 25% requirement under the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. As at 24 February 2026, the public float had further risen to approximately 26.05%.

1 The 0.75% Exchangeable Bonds are being accounted for as financial liabilities at fair value through profit or loss and are excluded from both the net debt and net gearing ratio calculations. If the 0.75% Exchangeable Bonds were included as debt, the net gearing ratio would be 39% as at 31 December 2025.

Business Performance Highlights

Roads

A stable performance despite a challenging environment

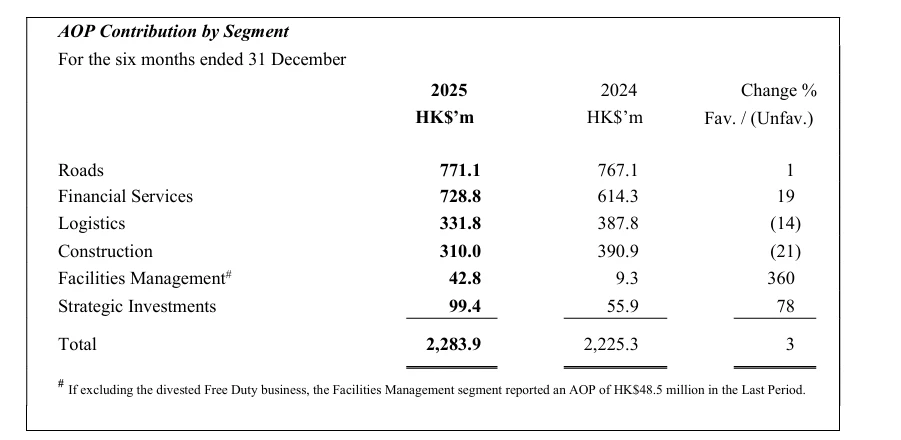

During the Current Period, the Roads segment recorded a modest year-on-year AOP increase of 1% to HK$771.1 million. This was attributable to lower finance costs, which were partially offset by uneven traffic recovery. However, like-for-like average daily traffic flow and toll revenue both declined 1% year-on-year, mainly due to partial closures on Beijing-Zhuhai Expressway (Guangzhou-Zhuhai Section) and Guangzhou-Zhaoqing Expressway during their ongoing expansion works. As at 31 December 2025, the road portfolio’s average remaining concession period stood at approximately 11.4 years.

Financial Services

Strong AOP and CSM Growth Momentum

In 1HFY2026, the Financial Services segment recorded a robust 19% year on year increase in AOP to HK$728.8 million, primarily driven by strong performance of Chow Tai Fook Life Insurance Company Limited (“CTF Life”). Profitable new business growth and favourable financial market movements contributed to a 17% year on year increase in Contractual Service Margin (“CSM”) release to HK$664.6 million, which remained the major driver of AOP. As at 31 December 2025, the CSM balance (net of reinsurance) rose 18% to HK$10.8 billion compared with 30 June 2025, reflecting positive financial market movements, solid new business momentum, and supporting a continued build-up of future earnings.

CTF Life achieved robust business growth in the Current Period, with Annual Premium Equivalent (“APE”) increased 48% year-on-year to HK$2,287.8 million. Agency channel has grown significantly, with its APE rising 32% year-on-year, driven by a 24% year-on-year uplift in productivity. Agency channel’s persistency ratio improved by 13% year-on-year. The partnership channel also delivered strong momentum, with APE up 78% year on year.

Value of New Business (“VONB”) continued to expand in line with APE growth, increasing 39% to HK$733.3 million during the Current Period. VONB margin improved from 27% in the first half of 2025 to 32% in the Current Period, due to higher premium growth and improved cost efficiency.

CTF Life also maintained a strong financial position. As at 31 December 2025, its solvency ratio under the Hong Kong Risk Based Capital regime stood at 282%, well above the minimum regulatory requirement of 100%. As at 31 December 2025, embedded value increased by 10% from 30 June 2025 to HK$27.8 billion. CTF Life’s market position ranking 12th among life insurers in Hong Kong by APE in the first nine months of 2025.

Logistics

Diversified logistics investments across Greater China

The Logistics segment reported total AOP of HK$331.8 million for the Current Period, representing a 14% year-on-year decline. While China United International Rail Containers Co., Limited (“CUIRC”) delivered solid growth, this was offset by declining profits from ATL Logistics Centre Hong Kong Limited (“ATL”) in Hong Kong and logistics properties in the Chinese Mainland.

As at 31 December 2025, ATL recorded a year-on-year average rental growth of 3%, offset by a decline in occupancy to 75.2% (30 June 2025: 80.7%). As the logistics industry continues to recover, the Group’s logistics assets in the Chinese Mainland recorded an increase in average occupancy rate. As at 31 December 2025, the average occupancy rate across the seven logistics assets in Chengdu, Wuhan, and Suzhou rose to 90.9% (30 June 2025: 87.5%). In pursuit of strengthening its logistics asset network and enhancing synergies across the Chinese Mainland, the Group completed the acquisition of a logistics property in Dongguan in December 2025. Following this addition, the overall average occupancy rate across the eight logistics assets in Chengdu, Wuhan, Suzhou and Dongguan stood at 91.2% as at 31 December 2025.

CUIRC achieved notable year-on-year AOP growth of 19% during the Current Period. Throughput rose by 10% year-on-year to 3,842,000 TEUs.

Construction

Delivering long‑term value through proven construction expertise

CTFS Construction Group comprises four well-established professional entities: Hip Hing Group, Vibro Group, Quon Hing Group, and Hsin Chong Aster, offering an integrated one-stop solution to clients. As at 31 December 2025, newly secured contracts surged by 115% year-on-year to HK$9.7 billion, lifting the gross value of contracts on hand to approximately HK$65.4 billion. Remaining works to be completed also increased to HK$39.6 billion as at 31 December 2025, providing visibility for future revenue.

Major contracts awarded during the Current Period included design and build of joint-user complex, public open space at Cheung Sha Wan Road, Sham Shui Po, construction of public housing development at Yip On Factory Estate and management contract for maintenance and completion works for the subsidized sale flats development at Anderson Road Quarry Site R2-2.

Despite the strengthened order book and solid project delivery, AOP declined 21% year-on-year to HK$310.0 million, mainly due to lower gross margins recognized from projects during the Current Period and the absence of Last Period’s reversals of expected credit loss provision, leading to a contraction in overall net profit margins.

Facilities Management

Manage & operate iconic facilities in HK

The Facilities Management segment recorded a year-on-year increase of 360% to HK$42.8 million in the Current Period. Excluding the Free Duty business which was divested in December 2024, the segment reported a year-on-year AOP decline of 12%.

Gleneagles Hospital Hong Kong (“GHK”) contributed positively to the Group’s profitability, delivering sustained solid growth and making a turnaround from AOL in the Last Period. This was partially offset by the decline in AOP from the Hong Kong Convention and Exhibition Centre (“HKCEC”) and an AOL incurred by Kai Tak Sports Park Limited (“KTSPL”), in which the Group holds a 25% interest, during the ramp-up phase of Kai Tak Sports Park (“KTSP”).

GHK reported an AOP in the Current Period compared with an AOL in the Last Period. Revenue recorded steady growth, and EBITDA increased by 11% year-on-year. The number of inpatients, outpatients and day cases rose by 1%, 2% and 8%, respectively. As at 31 December 2025, the number of regularly utilized beds increased to 352 (30 June 2025: 337), with an average occupancy rate of 58% (30 June 2025: 64%).

To support GHK’s service offerings and long-term development roadmap, Parkway Medical Services (Hong Kong) Limited, a business venture between the Group and IHH Healthcare Berhad, continued to expand its integrated healthcare network. In October 2025, Gleneagles MediCentre opened in Admiralty, increasing the total number of clinics and service centres to eight.

Due to increased depreciation and higher capital expenditure, subdued food and beverage revenue as a result of fewer events, HKCEC recorded a decline in AOP with a 4% year-on-year decrease in total attendance, reaching approximately 4.4 million across 378 events (Last Period: 426). The venue remains committed to delivering premium services and facilities to event organizers and continues to attract a diverse portfolio of events.

KTSP hosted 29 sports events and 11 entertainment events during the Current Period, attracting approximately over 7 million visitors precinct wide. According to leading industry magazine Pollstar, KTSP ranked third globally and first in Asia in ticket sales for 2025, despite having only opened in March 2025 while other venues reported a full year of operations. In addition, the 700,000-square-foot retail mall, Kai Tak Mall, achieved an occupancy rate of approximately 90% as at 31 December 2025.

Outlook

In FY2026, the Group maintains a positive outlook, supported by its diversified business portfolio and strong financial foundation. The re-inclusion into the Hang Seng Composite Index, effective 9 March 2026, which makes the Company eligible for both the Shanghai‑Hong Kong Stock Connect and the Shenzhen‑Hong Kong Stock Connect programmes. Participation in these programmes, if approved, would broaden Chinese Mainland investor access, enhance share liquidity, and strengthen overall market visibility.

Looking ahead, the Group will continue to respond with agility to external developments, leveraging its solid balance sheet and operational discipline to capture opportunities and deliver sustainable value to shareholders.

HIGHLIGHTS

- Profit attributable to shareholders of the Company rose 15% year-on-year to HK$1,334.3 million.

- Overall Attributable Operating Profit (“AOP”) delivered a steady growth of 3% year-on-year to HK$2,283.9 million.

- The Group’s financial position remained solid. Total available liquidity stood at approximately HK$31.0 billion as at 31 December 2025, comprising cash and bank balances of approximately HK$20.9 billion and unutilized committed banking facilities of approximately HK$10.1 billion.

- Prudent and proactive balance sheet management. As at 31 December 2025, the Group’s debt due within one year lowered 28% to HK$6.8 billion, with net debt reduced 6% to HK$13.8 billion, and net gearing ratio reduced to 34%.

- Committed to sustainable and progressive dividend policy. The Group’s Interim Dividend is HK$0.28 per share (representing an approximate 3% year-on-year increase on a comparable basis, after adjusting FY2025 interim ordinary dividend to reflect the enlarged share capital base following the 1-for-10 bonus issue in December 2025). The total interim ordinary dividend amount rose by approximately 6% to HK$1.27 billion.

Mr Brian Cheng, Executive Director and Group Co-Chief Executive Officer of CTFS, said, “CTFS has delivered resilient performance with solid growth, underscoring the strength of our diversified business portfolio. We are advancing in our Financial Services and Logistics segments, with recent acquisitions driving strategic expansion and strengthening our market position, marking key milestones in our roadmap. We remain focused on strengthening portfolio resilience and maximizing synergies with the Chow Tai Fook Group, while seizing quality growth opportunities at the right time to drive sustainable, long‑term value creation.”

Mr Gilbert Ho, Executive Director and Group Co-Chief Executive Officer of CTFS, added, “CTFS will continue to pursue disciplined growth, anchored by prudent approach to capital and risk management. Backed by a strong balance sheet and commitment to operational excellence, we are well‑positioned to navigate evolving market conditions. By optimizing our portfolio and enhancing efficiency, we reinforce cash flow resilience and deliver stable performance, enabling us to uphold a sustainable and progressive dividend policy across market cycles.”

Disciplined Capital Allocation

Strategic Divestment and Acquisitions

The Group applied a disciplined approach to capital allocation, balancing strategic divestments of stagnant assets and targeted investments in areas of clear strategic importance. In October 2025, the Group monetized its investment in Shoucheng Holdings Limited under the Strategic Investment segment through the issuance of HK$2,218 million 0.75% exchangeable bonds due 2028 (the “0.75% Exchangeable Bonds”). This transaction enables the Group to diversify its funding source and strengthen its financial flexibility to support future growth initiatives while potentially divest the investment with an attractive return.

The Group also advanced selective acquisitions to reinforce its core business segments, including the following:

Financial Services:

- Announced acquisition of a 65% interest in Blackhorn Group Limited (“Blackhorn”), an external asset manager. (August 2025)

- Completed acquisition of 13.05% stake in uSmart Inlet Group Ltd (“uSMART”), a technology-driven financial services provider. (November 2025)

Logistics:

- Completed acquisition of a logistics property in Dongguan (December 2025)

- Completed acquisition of three logistics properties in the Yangtze River Delta after the reporting period (January 2026)

Proactive Financial Management Strengthens Liquidity

Strengthening Liquidity and Reducing Leverage Level

The Group maintains a solid financial position. As at 31 December 2025, total available liquidity amounted to approximately HK$31.0 billion, comprising cash and bank balances of approximately HK$20.9 billion and unutilized committed banking facilities of approximately HK$10.1 billion, comfortably exceeding near-term maturities. As at 31 December 2025, net debt declined to approximately HK$13.8 billion (30 June 2025: approximately HK$14.7 billion), with the net gearing ratio, calculated as net debt over total equity, further edged down to 34%1 (30 June 2025: 37%). The Group reduced its average borrowing costs to approximately 4.0% per annum (for the six months ended 31 December 2024 (the “Last Period”): 4.2% per annum).

During the Current Period, the Company successfully increased its public float to meet the regulatory requirement. In July 2025, the Company issued HK$850 million of 2.80% convertible bonds due 2027. Subsequent conversions lifted public float to approximately 25.08% as at 21 November 2025, complying with the minimum 25% requirement under the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. As at 24 February 2026, the public float had further risen to approximately 26.05%.

1 The 0.75% Exchangeable Bonds are being accounted for as financial liabilities at fair value through profit or loss and are excluded from both the net debt and net gearing ratio calculations. If the 0.75% Exchangeable Bonds were included as debt, the net gearing ratio would be 39% as at 31 December 2025.

Business Performance Highlights

Roads

A stable performance despite a challenging environment

During the Current Period, the Roads segment recorded a modest year-on-year AOP increase of 1% to HK$771.1 million. This was attributable to lower finance costs, which were partially offset by uneven traffic recovery. However, like-for-like average daily traffic flow and toll revenue both declined 1% year-on-year, mainly due to partial closures on Beijing-Zhuhai Expressway (Guangzhou-Zhuhai Section) and Guangzhou-Zhaoqing Expressway during their ongoing expansion works. As at 31 December 2025, the road portfolio’s average remaining concession period stood at approximately 11.4 years.

Financial Services

Strong AOP and CSM Growth Momentum

In 1HFY2026, the Financial Services segment recorded a robust 19% year on year increase in AOP to HK$728.8 million, primarily driven by strong performance of Chow Tai Fook Life Insurance Company Limited (“CTF Life”). Profitable new business growth and favourable financial market movements contributed to a 17% year on year increase in Contractual Service Margin (“CSM”) release to HK$664.6 million, which remained the major driver of AOP. As at 31 December 2025, the CSM balance (net of reinsurance) rose 18% to HK$10.8 billion compared with 30 June 2025, reflecting positive financial market movements, solid new business momentum, and supporting a continued build-up of future earnings.

CTF Life achieved robust business growth in the Current Period, with Annual Premium Equivalent (“APE”) increased 48% year-on-year to HK$2,287.8 million. Agency channel has grown significantly, with its APE rising 32% year-on-year, driven by a 24% year-on-year uplift in productivity. Agency channel’s persistency ratio improved by 13% year-on-year. The partnership channel also delivered strong momentum, with APE up 78% year on year.

Value of New Business (“VONB”) continued to expand in line with APE growth, increasing 39% to HK$733.3 million during the Current Period. VONB margin improved from 27% in the first half of 2025 to 32% in the Current Period, due to higher premium growth and improved cost efficiency.

CTF Life also maintained a strong financial position. As at 31 December 2025, its solvency ratio under the Hong Kong Risk Based Capital regime stood at 282%, well above the minimum regulatory requirement of 100%. As at 31 December 2025, embedded value increased by 10% from 30 June 2025 to HK$27.8 billion. CTF Life’s market position ranking 12th among life insurers in Hong Kong by APE in the first nine months of 2025.

Logistics

Diversified logistics investments across Greater China

The Logistics segment reported total AOP of HK$331.8 million for the Current Period, representing a 14% year-on-year decline. While China United International Rail Containers Co., Limited (“CUIRC”) delivered solid growth, this was offset by declining profits from ATL Logistics Centre Hong Kong Limited (“ATL”) in Hong Kong and logistics properties in the Chinese Mainland.

As at 31 December 2025, ATL recorded a year-on-year average rental growth of 3%, offset by a decline in occupancy to 75.2% (30 June 2025: 80.7%). As the logistics industry continues to recover, the Group’s logistics assets in the Chinese Mainland recorded an increase in average occupancy rate. As at 31 December 2025, the average occupancy rate across the seven logistics assets in Chengdu, Wuhan, and Suzhou rose to 90.9% (30 June 2025: 87.5%). In pursuit of strengthening its logistics asset network and enhancing synergies across the Chinese Mainland, the Group completed the acquisition of a logistics property in Dongguan in December 2025. Following this addition, the overall average occupancy rate across the eight logistics assets in Chengdu, Wuhan, Suzhou and Dongguan stood at 91.2% as at 31 December 2025.

CUIRC achieved notable year-on-year AOP growth of 19% during the Current Period. Throughput rose by 10% year-on-year to 3,842,000 TEUs.

Construction

Delivering long‑term value through proven construction expertise

CTFS Construction Group comprises four well-established professional entities: Hip Hing Group, Vibro Group, Quon Hing Group, and Hsin Chong Aster, offering an integrated one-stop solution to clients. As at 31 December 2025, newly secured contracts surged by 115% year-on-year to HK$9.7 billion, lifting the gross value of contracts on hand to approximately HK$65.4 billion. Remaining works to be completed also increased to HK$39.6 billion as at 31 December 2025, providing visibility for future revenue.

Major contracts awarded during the Current Period included design and build of joint-user complex, public open space at Cheung Sha Wan Road, Sham Shui Po, construction of public housing development at Yip On Factory Estate and management contract for maintenance and completion works for the subsidized sale flats development at Anderson Road Quarry Site R2-2.

Despite the strengthened order book and solid project delivery, AOP declined 21% year-on-year to HK$310.0 million, mainly due to lower gross margins recognized from projects during the Current Period and the absence of Last Period’s reversals of expected credit loss provision, leading to a contraction in overall net profit margins.

Facilities Management

Manage & operate iconic facilities in HK

The Facilities Management segment recorded a year-on-year increase of 360% to HK$42.8 million in the Current Period. Excluding the Free Duty business which was divested in December 2024, the segment reported a year-on-year AOP decline of 12%.

Gleneagles Hospital Hong Kong (“GHK”) contributed positively to the Group’s profitability, delivering sustained solid growth and making a turnaround from AOL in the Last Period. This was partially offset by the decline in AOP from the Hong Kong Convention and Exhibition Centre (“HKCEC”) and an AOL incurred by Kai Tak Sports Park Limited (“KTSPL”), in which the Group holds a 25% interest, during the ramp-up phase of Kai Tak Sports Park (“KTSP”).

GHK reported an AOP in the Current Period compared with an AOL in the Last Period. Revenue recorded steady growth, and EBITDA increased by 11% year-on-year. The number of inpatients, outpatients and day cases rose by 1%, 2% and 8%, respectively. As at 31 December 2025, the number of regularly utilized beds increased to 352 (30 June 2025: 337), with an average occupancy rate of 58% (30 June 2025: 64%).

To support GHK’s service offerings and long-term development roadmap, Parkway Medical Services (Hong Kong) Limited, a business venture between the Group and IHH Healthcare Berhad, continued to expand its integrated healthcare network. In October 2025, Gleneagles MediCentre opened in Admiralty, increasing the total number of clinics and service centres to eight.

Due to increased depreciation and higher capital expenditure, subdued food and beverage revenue as a result of fewer events, HKCEC recorded a decline in AOP with a 4% year-on-year decrease in total attendance, reaching approximately 4.4 million across 378 events (Last Period: 426). The venue remains committed to delivering premium services and facilities to event organizers and continues to attract a diverse portfolio of events.

KTSP hosted 29 sports events and 11 entertainment events during the Current Period, attracting approximately over 7 million visitors precinct wide. According to leading industry magazine Pollstar, KTSP ranked third globally and first in Asia in ticket sales for 2025, despite having only opened in March 2025 while other venues reported a full year of operations. In addition, the 700,000-square-foot retail mall, Kai Tak Mall, achieved an occupancy rate of approximately 90% as at 31 December 2025.

Outlook

In FY2026, the Group maintains a positive outlook, supported by its diversified business portfolio and strong financial foundation. The re-inclusion into the Hang Seng Composite Index, effective 9 March 2026, which makes the Company eligible for both the Shanghai‑Hong Kong Stock Connect and the Shenzhen‑Hong Kong Stock Connect programmes. Participation in these programmes, if approved, would broaden Chinese Mainland investor access, enhance share liquidity, and strengthen overall market visibility.

Looking ahead, the Group will continue to respond with agility to external developments, leveraging its solid balance sheet and operational discipline to capture opportunities and deliver sustainable value to shareholders.

-END-

PDF